- You are here:

-

Home

-

Research, Analysis & Trends

- IDC’s big data and analytics spending guide

According to the latest release of IDC's Worldwide Big Data and Analytics (BDA) Spending Guide, spending on BDA solutions will grow by 19% in the Asia Pacific region in 2022 and will rise 1.6 times to $53.3 billion by 2025. Enterprises' evolving need to gain operational efficiency and operational resilience is driving investments. Building operational resilience stems from providing a real-time response to external market disruptions such as the pandemic, supply chain vulnerabilities, or rapidly evolving customer needs.

According to the latest release of IDC's Worldwide Big Data and Analytics (BDA) Spending Guide, spending on BDA solutions will grow by 19% in the Asia Pacific region in 2022 and will rise 1.6 times to $53.3 billion by 2025. Enterprises' evolving need to gain operational efficiency and operational resilience is driving investments. Building operational resilience stems from providing a real-time response to external market disruptions such as the pandemic, supply chain vulnerabilities, or rapidly evolving customer needs.

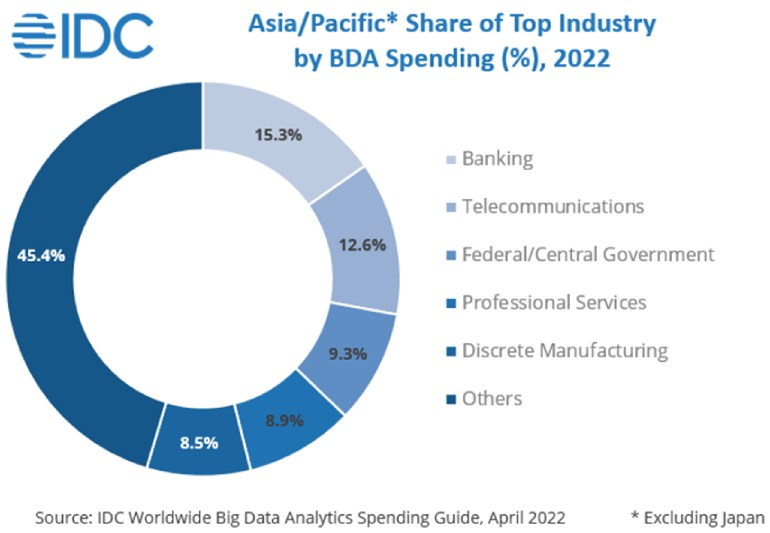

“From covid to the Russia-Ukraine war, the level of disruptions that we have experienced in the past two years have been unprecedented,” says Jessie Danqing Cai, Associate Research Director at IDC Asia/Pacific, Big Data & Analytics Practice. “Organizations need to have a clear strategy to extract value from their data asset, to enable evidence-based decision making, data science explorations, and actionable insight delivery at scale,” Cai adds. Over the next five years, banking will continue to be the largest investor in big data analytics solutions, capturing 15.3% in 2022, the highest BDA spending, focusing on fraud detection and improved customer experience to ensure increased customer loyalty.

Over the next five years, banking will continue to be the largest investor in big data analytics solutions, capturing 15.3% in 2022, the highest BDA spending, focusing on fraud detection and improved customer experience to ensure increased customer loyalty.

Second, telecommunication will retain its position across the forecasted period ending in 2025. At 12.6% in 2022, investments are directed toward infrastructure and networks to generate insight to improve the efficiency and effectiveness of network operations, improve throughput, and reduce downtime. Both these industries will grow with a CAGR (2020–2025) exceeding 17% over the forecast period.

The federal and central government's focus on critical infrastructure management and health/wellness monitoring will lead investment to grow by 16% until the end of the forecast period. The top four industries, banking, telecommunication, federal/central government, and professional services registered cumulative spending of $15.0 billion, nearly 46% of the total spending share in 2022 captured by the 19 industries mapped by IDC.

"Organizations’ priority area for investment in data and analytics varies by industry," says Abhik Sarkar, Market Analyst at IDC Asia/Pacific IT Spending Guides, Customer Insights & Analysis. "Finance and government sectors prioritize automation and cybersecurity, while retail and wholesale focus more on customer experience, and manufacturing focuses on worker productivity/quality. Hence, it is imperative that vendors target outcomes of their solutions by industries," Sarkar adds.

The services technology group captured the highest spending share at 43.4% in 2022 followed by software, then hardware. For the software technology group, content analytics tools, continuous analytics tools, and nonrelational analytics tools are the major technology categories driving spending growth. By deployment type, the on-premises deployment type captured a maximum revenue share of $6.0 billion in 2022. However, this trend is expected to change in the future with Public Cloud Services capturing a lion’s share of the spending at 52.6% in 2025 at $9.17 billion.

By MediaBUZZ